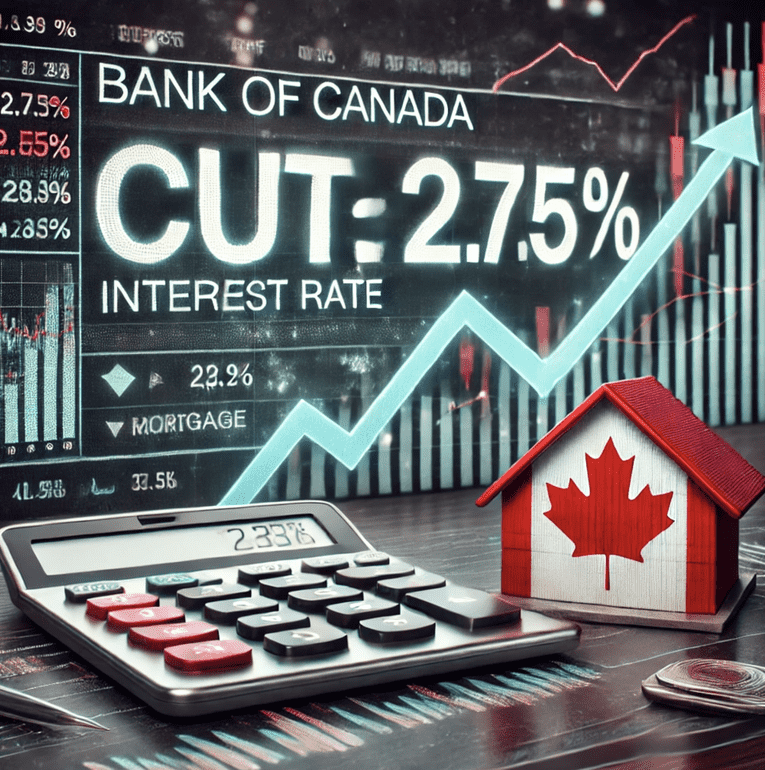

Bank of Canada Cuts Rates to 2.75% – What It Means for Prime & Variable Rates

The Bank of Canada announced another rate cut this morning, lowering its key interest rate by 0.25% to 2.75%. This move comes as global economic uncertainty rises, with former U.S. President Donald Trump escalating his tariff war, adding pressure on central banks to adjust their monetary policies.

Impact on Prime Rate

With this rate cut, Canada’s prime lending rate is expected to decrease from 5.20% to 4.95%. The prime rate is the benchmark banks use to set interest rates for various loans, including variable-rate mortgages, home equity lines of credit (HELOCs), and business loans.

For borrowers, this means slightly lower monthly payments on loans tied to the prime rate. Homeowners with variable-rate mortgages will see some relief in their mortgage payments, though the actual impact depends on the lender’s adjustments. Those considering borrowing may find financing slightly more affordable, encouraging economic activity.

Why the Rate Cut Now?

The Bank of Canada’s decision reflects concerns over economic growth, inflation, and the impact of global trade tensions. With Trump’s aggressive tariff policies increasing economic uncertainty, the central bank is taking a proactive approach to support borrowing and investment.

What’s Next?

Economists are watching closely to see if further cuts will follow. If economic pressures persist, the Bank of Canada may continue adjusting rates to maintain stability and growth.

For mortgage holders and prospective buyers, this could be an opportunity to explore refinancing options or lock in favorable rates before further changes occur.

Stay informed, and if you have questions about how this affects your mortgage, consult with a financial expert to make the best decision for your situation.

Each Office is Independently Owned & Operated • Brokerage 13072 | © Copyright 2024 . All Rights Reserved